If you’re planning to buy a home but worried about the upfront costs, you may be asking: who qualifies for down payment assistance? The good news is that thousands of buyers across the U.S. benefit from these programs every year—including first-time buyers, veterans, teachers, and moderate-income households.

Qualifying isn’t as difficult as it may seem, and understanding the eligibility requirements is your first step toward accessing free or low-cost assistance for down payment and closing costs.

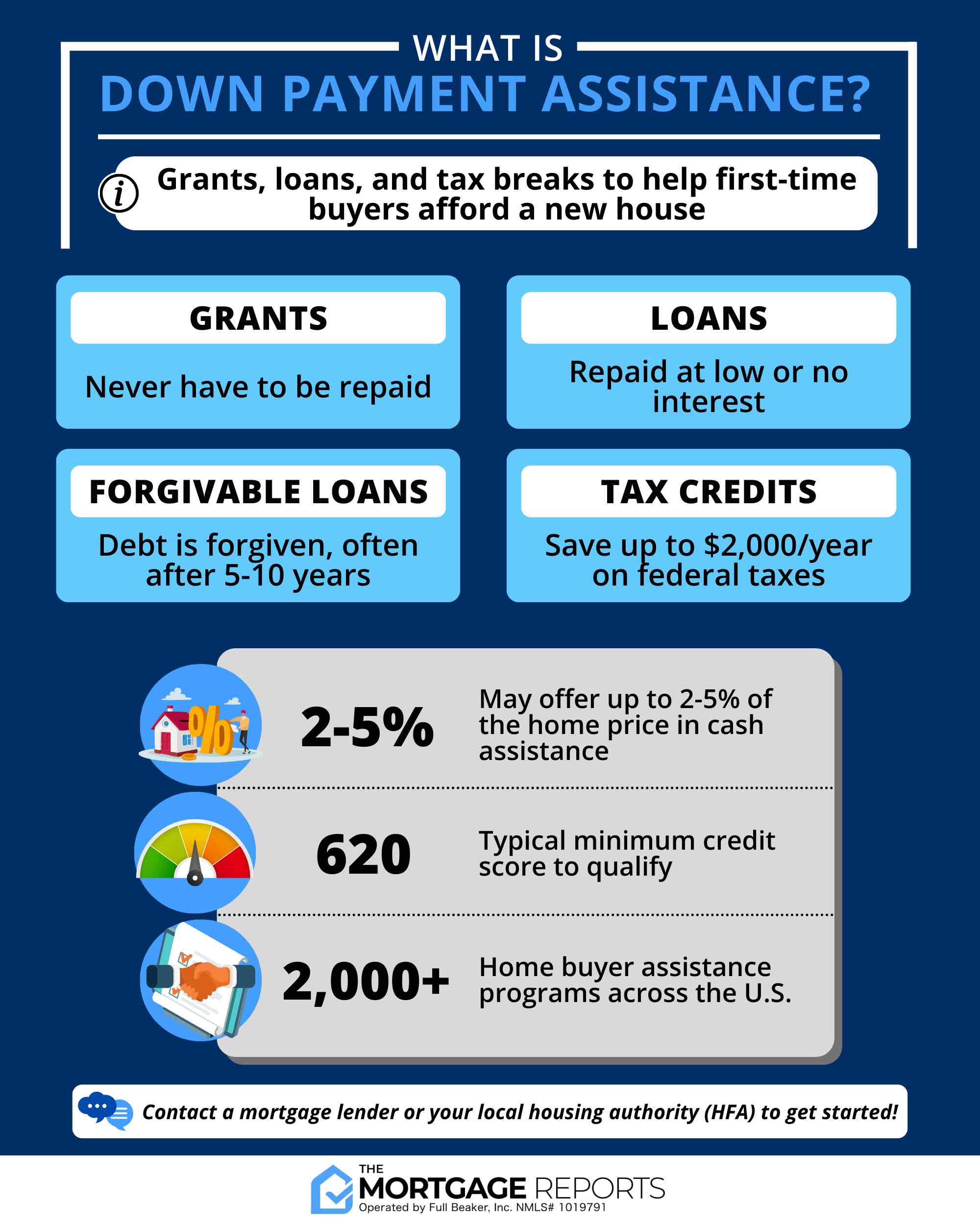

✅ General Requirements for DPA Eligibility

While criteria vary by state and program, most down payment assistance (DPA) programs share the following basic requirements:

- 👨👩👧👦 Be a first-time homebuyer (or not have owned a home in the last 3 years)

- 🏠 Use the home as your primary residence

- 📍 Buy within the geographic area covered by the program

- 📉 Meet income limits based on family size and location

- 💼 Apply through an approved lender

- 📘 Complete a homebuyer education course

📊 Income Limits – What You Need to Know

Most DPA programs set income limits tied to the Area Median Income (AMI) where the home is located. These limits may range from 80% to 120% of AMI.

For example:

- 🧑 Single person in Phoenix, AZ: limit may be ~$66,000

- 👨👩👧👦 Family of 4 in Dallas, TX: limit may be ~$98,000

Your lender will check the latest limits for your county when you apply.

🏡 Property Requirements

To qualify for DPA, the home must generally:

- ✅ Be a single-family home, condo, or townhouse

- 📍 Be located within the approved city/county/state

- 🔧 Meet basic habitability standards

- 💲 Fall within the program’s purchase price cap

🎓 Education Requirements

Most programs require buyers to take a HUD-approved homebuyer education course before closing. These courses cover topics like:

- 📈 Budgeting for homeownership

- 🏦 Understanding mortgage terms

- 🔧 Maintenance responsibilities

💼 Employment and Loan Type

While not always required, some programs give priority or additional options to:

- 👩🏫 Teachers, first responders, healthcare workers

- 🎖 Veterans and active military

- 👷 Workers in high-need sectors or rural areas

In terms of mortgage loan types, DPA can usually be combined with:

- FHA loans

- VA loans

- USDA loans

- Conventional loans (e.g., Fannie Mae HFA Preferred)

🔁 First-Time Buyer Rule Exceptions

Many DPA programs define “first-time homebuyer” as someone who hasn’t owned a home in the past 3 years. You may also qualify if:

- 🧓 You are a divorced or displaced homemaker

- 🏚 You’re purchasing in a targeted revitalization area

- 🎖 You are a qualified veteran

🔍 Buyer Story Example

Erica, a childcare worker in Ohio, qualified for $7,500 in assistance through a state program even though she wasn’t a first-time buyer—because her new home was in a designated target area. Her credit was average, but her income and education completion made her eligible.

📍 Where to Check Eligibility by State

- 💵 Texas Down Payment Assistance

- 🌴 Florida DPA Programs

- 🏘️ Ohio Homebuyer Assistance

- 🏔️ Colorado DPA Programs

📥 Want to Know If You Qualify?

The fastest way to know if you qualify is to talk to a lender approved by your state housing agency. They’ll help determine your eligibility based on income, credit, location, and loan type.

📍 Check Local Programs by State (via HUD)